After several years of recovery, the U.S. offshore support vessel (OSV) market has settled into a steadier phase.

Activity across the Gulf of Mexico (renamed by the Trump administration as the Gulf of America) remains consistent, with vessels supporting drilling campaigns, subsea work, and ongoing maintenance programs. Compared with the prolonged downturn that defined much of the previous decade, conditions are meaningfully stronger, but the engine driving that strength has changed.

For a time, the driver was a backlog of work built up during the Covid-19 pandemic. As that backlog cleared, activity crested around 2023 and has since leveled off. What remains is a market running on its underlying fundamentals rather than deferred demand.

Those fundamentals, however, are shifting. Offshore energy developers are gravitating toward smaller, incremental developments. Fewer large-scale projects are being sanctioned. And the fleet supporting that work is aging in place, with essentially no newbuild activity to refresh it.

The floor has held. The ceiling has not moved.

POST-COVID SURGE

In the years immediately following the pandemic, offshore operators moved quickly to complete work that had been delayed. “They were in a rush to execute what had not been carried out,” said Jean-Baptiste Rougeot, market intelligence lead at maritime data provider Spinergie. “Operators were booking vessels on both short- and long-term contracts to complete deferred work.”

That push created a temporary surge in demand, driven less by new investment and more by the need to catch up.

As those projects were completed, activity settled into a more normalized pattern. The backlog that sustained the recovery has largely worked through the system, and the market is no longer benefiting from the same surge of deferred work.

Simultaneously, investment in new large-scale offshore developments has remained limited. Fewer final investment decisions, particularly in deepwater projects, have narrowed the pipeline of future work.

PROJECT MIX

The change is most visible in the type of offshore work now moving forward. Large developments once requiring sustained vessel support are giving way to smaller projects that can be brought online more quickly. In particular, tieback developments, which connect new wells to existing infrastructure, have become a larger share of activity.

“A tieback can require 10 times fewer vessels than a large greenfield project,” Rougeot said.

Work continues across the Gulf, but jobs are often shorter in duration and less vessel intensive. The number of major deepwater developments moving forward each year has declined, reducing the volume of work that typically supports long-term vessel demand.

That shift does not reduce activity outright. It changes how much support activity is required and, in turn, the types of vessels operators are prioritizing. Work tied to shorter-duration projects is increasingly aligned with vessels capable of subsea support rather than large-scale construction, a trend reflected in recent fleet investments across the Gulf.

HIGH-SPEC DEMAND

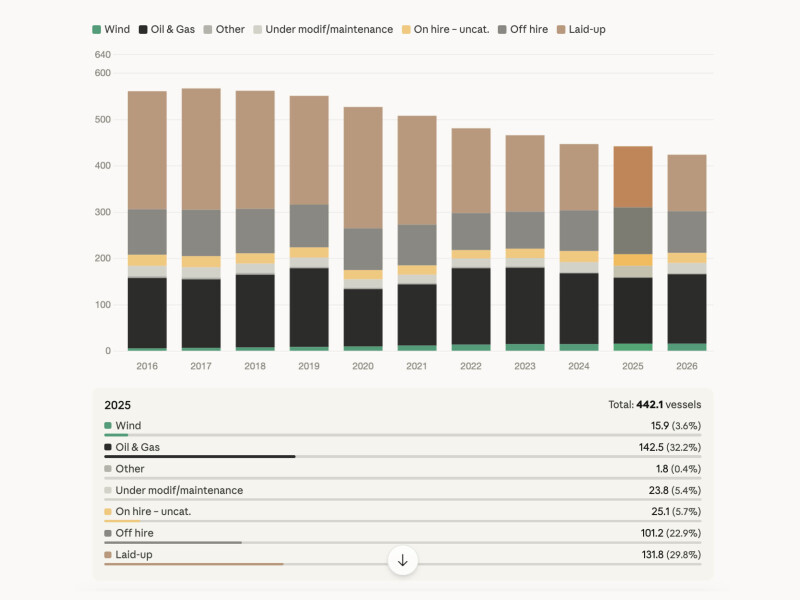

On paper, the OSV market still appears to have available capacity. A significant portion of the fleet is either off-hire or working intermittently, based on vessel activity tracked across the year. That suggests additional vessels could be brought back into service if demand increases. According to Spinergie, roughly 25% of the global OSV fleet was off hire in 2025, with additional vessels laid up.

In the U.S. Gulf, much of that available capacity is constantly moving between on- and off-hire status. “The U.S. Gulf is a spot market,” Rougeot said. “Vessels move in and out of work depending on short-term demand.”

The result is a supply picture that looks flexible but is less reliable in practice. Not every vessel labeled as technically available is ready to return to service or suited to current project requirements.

Availability and usable capacity are not the same. As work becomes more specialized, that distinction becomes more important. Much of the activity now moving through the Gulf requires higher-spec vessels equipped for subsea operations, survey, and inspection, limiting how much of the existing fleet can realistically step into active roles, according to Rougeot.

AGING FLEET

The most significant pressure on the OSV market is not on the demand side. It is the condition of the fleet itself, Rougeot said. In North America, Spinergie data shows more than 60% of OSVs are now more than 15 years old, approaching or exceeding what is typically considered a 15- to 20-year operational life, though Jones Act vessels have routinely proven useful well beyond that threshold. “The fleet is aging, and that will be the main challenge in the coming years,” Rougeot said.

While older tonnage can get the job done, aging vessels are more difficult to maintain, less efficient to operate, and harder to bring back into service after being laid up. The industry has long relied on stacking and reactivation to manage swings in demand, which becomes less effective as vessels get older.

“A vessel that is stacked will age faster than one that is operating,” Rougeot said.

The constraint limits how much of the existing fleet can realistically be reactivated, even if demand increases. In response, operators are investing in vessels that can meet evolving technical requirements. Morrison, Houma, La., for example, recently added a dynamically positioned dive-support vessel (DSV) to expand its ability to operate in deeper water and on projects requiring station-keeping without mooring systems, a move driven by client demand for more advanced capabilities, the company said.

NO NEWBUILDS

Under normal conditions, an aging fleet would trigger a new cycle of vessel construction. That cycle has not materialized across the U.S. offshore fleet, and there is little sign it will anytime soon.

Construction costs have risen sharply, and charterers, meanwhile, are not committing to the kind of large, long-term deals that typically support newbuild investment. “Today, you don’t have the market conditions to build at a decent, profitable cost,” Rougeot said.

The scale problem compounds this further. U.S. operators typically cannot place the volume of orders needed to drive down unit costs, while international competitors building in larger batches can spread expenses across multiple hulls. Without a clear return on investment, capital has shifted toward acquiring and upgrading existing vessels rather than commissioning new ones, a trend Rougeot said reflects both cost pressures and a lack of sustained demand. The industry is expected to rely on existing tonnage for the foreseeable future.

With OSV sector capital now flowing to acquisitions and upgrades, investments are focused on higher-spec assets that can support more complex work.

Recent transactions in the Gulf reflect that shift. Otto Candies LLC, Des Allemands, La., acquired four multipurpose support vessels from Harvey Gulf International Marine, New Orleans, in a deal valued at just under $500 million. The vessels — renamed Blue-Sea, Sub-Sea, Deep-Sea, and Intervention — were built between 2012 and 2017 and were secured at a price below current replacement cost. This highlights the gap between asset values and the cost of building new tonnage, which is shaping investment decisions across the sector, with operators able to acquire relatively modern, high-spec vessels at a fraction of what new construction would require, as Otto Candies executives noted in discussing the transaction.

Other operators are following a similar approach. Subsea services provider Aqueos Corp., Broussard, La., acquired the DSV Kelly Ann Candies after several years under charter, bringing a proven subsea asset into its fleet and reinforcing the value of vessels with established roles in construction and inspection work, according to the company.

Upgrades are also extending the life and capability of existing vessels. Morrison expanded its dive-support fleet with a dynamically positioned vessel for deeperwater operations, while Oceaneering International Inc., Houston, upgraded its Ocean Intervention II to support autonomous survey missions, allowing the vessel to carry out multiple survey functions simultaneously and improving efficiency across subsea operations.

The focus has shifted from adding vessels to drawing more out of the ones already in service.

OFFSHORE WIND

Offshore wind has introduced new activity into U.S. offshore markets, but its impact on OSV demand remains limited.

According to Spinergie, offshore wind accounted for the equivalent of 16 full-time OSVs in 2025, based on vessel utilization across the year. Even when expanded to include the broader offshore construction and service fleet, the total reaches 71 vessel equivalents.

“Offshore wind has increased its share of activity, but it is still not the majority,” Rougeot said. “The OSV market remains anchored in oil and gas. We are not expecting wind to pick up in the short term.”

Some vessels continue to move between oil and gas and wind projects, particularly as project timelines shift, with subsea and construction vessels deployed across both sectors.

Policy uncertainty and project delays have limited offshore wind’s ability to generate sustained vessel demand. For now, it remains a supplemental source of activity rather than a primary driver of the OSV market.

PROJECT INFLUENCE

With fewer large-scale developments moving forward, each project carries more influence.

The number of major offshore projects sanctioned in the U.S. has declined in recent years, reducing the volume of work that typically supports long-term vessel utilization. The market has shifted from several large developments annually to roughly one major project per year.

That change increases sensitivity to delays, cost pressures, and shifting investment priorities.

“The key question is whether new deepwater project investment returns,” Rougeot said. “We are watching whether new projects are sanctioned and whether exploration wells are successful, because that is what will drive future activity.”

Several developments remain under watch, including new exploration programs and potential final investment decisions tied to recent lease sales. The success of those efforts will determine how much new work enters the system.

Without a broader pipeline, gaps between projects become more likely, and their impact on vessel demand becomes more immediate.

AGING PLATFORMS

One area where activity is expected to grow is decommissioning. In the Gulf’s shallow-water fields, aging infrastructure is reaching the end of its operational life. Hundreds of platforms are approaching removal, creating a steady pipeline of work tied to plugging, abandonment, and subsea operations.

Those projects require vessel support for inspection, heavy lifting, diving, and related services. Vessels like the Kelly Ann Candies are already positioned for this type of work, supporting pipeline installation, inspection, and subsea construction activities that closely align with decommissioning demand.

“Decommissioning will become a more important part of the market as infrastructure ages,” Rougeot said.

Decommissioning work tends to be smaller in scope but more consistent in frequency, favoring operators with specialized vessels already positioned in the market rather than those relying on broader fleet availability, a pattern reflected in recent subsea-focused acquisitions and upgrades.

The Chouest Group, Cut Off, La., is among companies eyeing expansion into the sector. In March, it announced a deal to acquire Champagne Energy Solutions, Houma, La., a U.S. Gulf provider of decommissioning, plug and abandonment, and environmental services that operates a fleet of four DSVs and a pipelay barge. In announcing the acquisition, Chouest said, “Additional strategic acquisitions [are] expected in the near term as the company builds a fully integrated platform in this space.”

“We see decommissioning as one of the most important and fastest-growing segments of the offshore energy market,” the company’s executive vice president, Dino Chouest, said in a statement.

POISED FOR CHANGE

The U.S. OSV market is holding its position, but it is no longer expanding in the way it once was. Demand remains steady, but it is more selective. Supply exists, but much of the fleet is aging and not all of it can be readily returned to service. Operators are adjusting by extending the life of existing vessels, upgrading capabilities, and concentrating on assets that can support more specialized work.

What comes next depends on whether new deepwater projects move forward and whether the industry can continue to operate within the limits of the fleet it already has in service.